A friend of mine called me a few weeks ago genuinely confused.

His portfolio wasn’t down much. A couple of stocks had slipped. A few positions were sitting flat. Nothing that should have kept him up at night. But every morning he was checking his phone before his feet hit the floor. Red days felt like a personal attack. Green days felt borrowed – like the market was just being polite before taking it back.

He thought the problem was the market.

I looked at what he actually owned and realized the problem had nothing to do with the market. It had everything to do with how the portfolio was built. He’d never sat down and thought seriously about asset allocation strategy for investors at his stage of life. He’d just bought things. One at a time. Over several years. Each decision made sense when he made it. Together they made a mess.

That’s how most portfolios get built, by the way. Not by design. By accident.

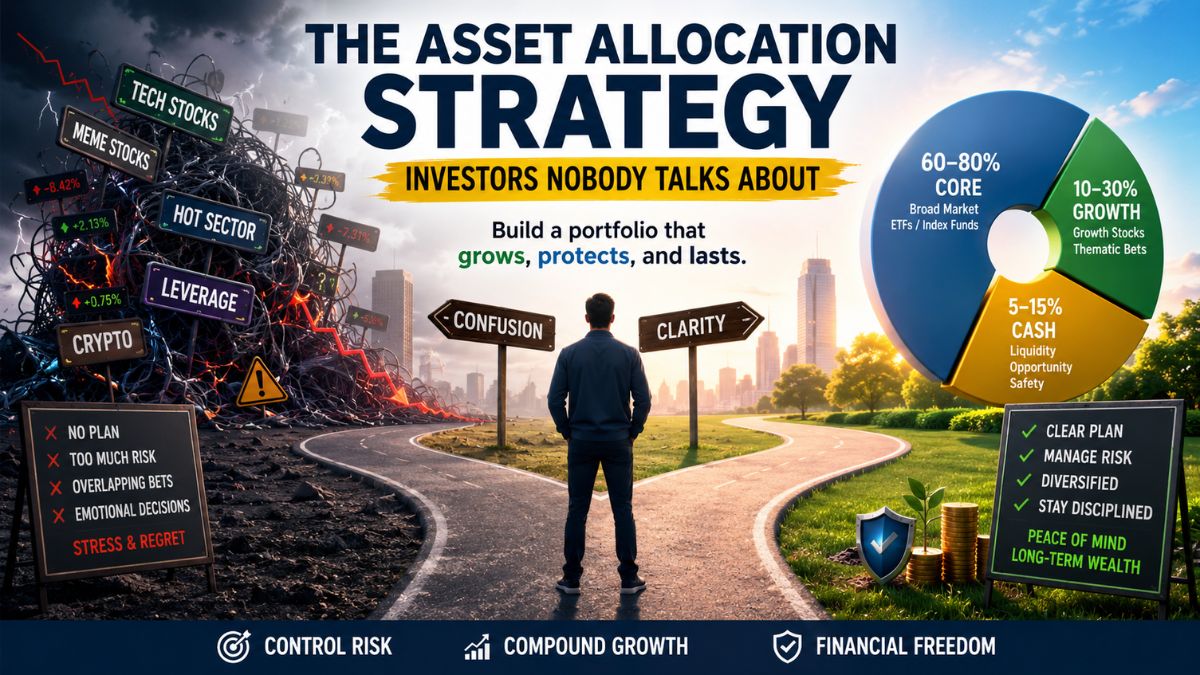

How Most Portfolios Become a Mess Without Anyone Noticing

Nobody sits down and says “I’m going to build a chaotic portfolio today.”

It happens in small steps. You hear about an AI stock at dinner and buy a few shares. A few weeks later a coworker mentions a cybersecurity company that’s “about to pop.” Then semiconductors start showing up in your feed. Then quantum computing. Then some speculative biotech that your brother-in-law has been watching for months and swears is different this time.

Suddenly you’ve got fourteen positions that are all quietly betting on the exact same thing – that the economy keeps growing, that investors stay optimistic, that technology spending doesn’t slow down. You think you’re diversified because the company names are different. You find out you weren’t when everything falls 20% in the same two weeks and there’s nowhere to hide.

That’s not diversification. That’s holding different versions of the same bet and calling it a strategy.

The correction doesn’t feel like bad luck at that point. It feels inevitable. Because it was.

What Your Risk Tolerance Actually Is vs. What You Think It Is

Most investors only discover their real risk tolerance when a correction actually arrives – and right now there are signals worth paying attention to. I recently broke down the Economic Collapse Warning Signs for 2026 that every self-directed investor should understand before the next move happens.

Here’s something I’ve noticed that nobody really wants to hear: most investors have no idea what their real risk tolerance is until money is actually disappearing – not dipping, disappearing.

During a bull market everyone is aggressive. Everyone can handle volatility. Everyone has conviction and a long time horizon and a plan for when things get rough.

Then a position falls 30%. A recession headline starts trending. Your account is down more than a few months of salary and it’s been that way for a while.

That’s when you find out who you actually are as an investor.

I’ve been through this myself. I thought I was genuinely comfortable with risk until I watched a position I believed in drop for four straight months. Not a bad week. Not a rough patch. Four months of opening the same app every morning and seeing a smaller number than the day before. Around month three I stopped having a logical reaction to it. I just felt dread.

That experience is what made me take asset allocation seriously for the first time. Because the right structure – one built before the stress arrives – forces you to answer hard questions while you’re still thinking clearly. How much can you actually lose without doing something emotional? How long can you hold something that looks wrong before you convince yourself the thesis is broken? What would you actually do if your portfolio dropped 40% in a single year and stayed there?

Most people skip those questions. Then they answer them badly at exactly the wrong moment.

Why Nobody Talks About This – And Why That’s Kind of the Point

“Expert Perspective: The Perfect Asset Allocation For 2026”

“If you want to dive deeper into how experienced investors are positioning themselves for the current market environment, I highly recommend watching this breakdown by Dr. Sven Carlin. He perfectly echoes the need for a resilient, long-term strategy over chasing short-term trends.”

Video Credit: Value Investing with Sven Carlin, Ph.D.

Watch more from Dr. Sven Carlin here

You will never see a finance influencer making a dramatic video about rebalancing into bonds.

Nobody goes viral talking about their cash position. There’s no screenshot-worthy moment when your diversified ETF quietly outperforms over a decade. The algorithm does not reward boring.

What gets attention is concentration. The guy who put everything into Nvidia in 2022 and held. The trader who turned $15,000 into $180,000 in eight months. Those stories spread because they’re extraordinary – and because the people telling them survived to tell them.

What doesn’t spread is the version of that story where it went the other way. Those investors just go quiet. You stop hearing from them. The forums move on.

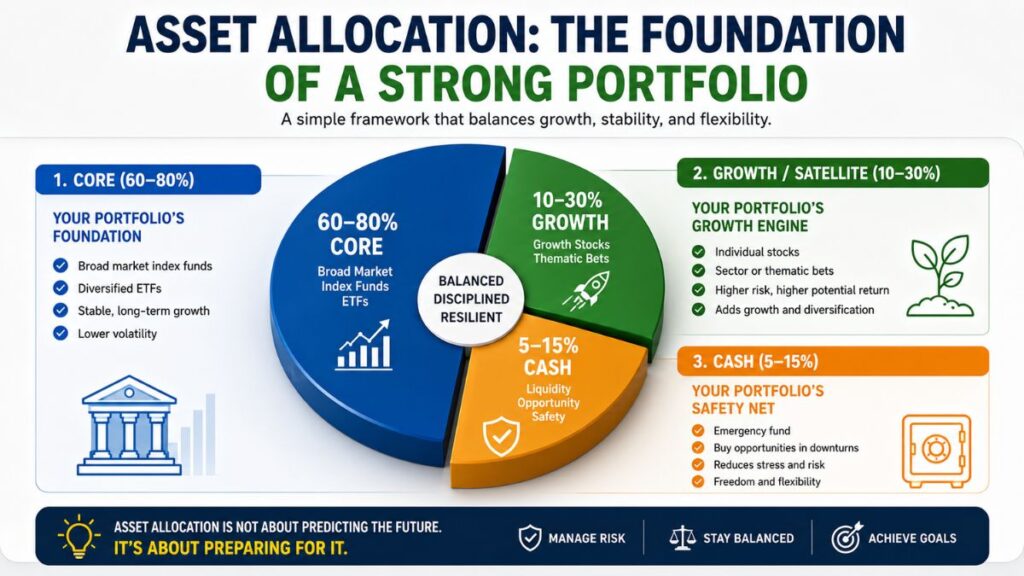

Asset allocation is boring by design. That’s not a flaw – it’s the entire purpose. Its job is making sure one bad call doesn’t undo years of progress. One over-hyped stock. One poorly timed trade. One sector that collapses the year you happened to be heavy in it. A real allocation strategy absorbs those hits instead of letting them define you.

Not exciting. Not shareable. Just the thing that’s still working ten years from now.

The Argument Smaller Portfolios Always Make

I hear this constantly from investors with under $100,000 in their accounts.

“Diversification won’t make me rich. I need to concentrate if I’m going to grow fast enough for it to matter.”

There’s something honest in that frustration. A broad index fund is not going to change your life in three years. I understand why that feels insufficient.

But concentrating doesn’t just increase your upside. It increases the speed at which things can go wrong. And the math of losses hits harder than most people realize until they live through it – if you lose 50% of your account, you need a 100% gain just to get back to where you started. Not 50%. One hundred percent.

The investors I’ve watched build real wealth over time are almost never the ones who made one spectacular bet. They’re usually the ones who didn’t blow themselves up during the three or four really ugly market periods that happened along the way. They stayed in the game long enough for compounding to actually work.

Boring is underrated. The problem is that boring requires patience, and patience has become one of the harder things to find in modern markets. We’ve been trained to expect fast feedback. The market is indifferent to that expectation.

Age Changes Everything and Most People Figure This Out Too Late

Not every portfolio looks the same – and for some investors, particularly those building around inflation protection or long-term store of value, alternative assets start to make sense. I recently covered why there is a growing Silver Investment Opportunity in 2026 worth understanding if that fits your allocation thinking.

This is where a lot of investing advice starts to fall apart. People want universal answers. They want a rule that works regardless of who you are or where you are in life.

There isn’t one.

A 26-year-old thinking about asset allocation strategy for investors just starting out is playing a completely different game than a 61-year-old who is three years from when they planned to stop working. The 26-year-old can make serious mistakes and recover. Markets cycle. Time heals most things in a portfolio. The 61-year-old doesn’t necessarily have that runway – a bad sequence of returns at the wrong moment can permanently change what retirement looks like.

That doesn’t mean older investors should avoid risk entirely. And it doesn’t mean younger investors should treat their brokerage account like a poker table. It means the timeline you’re actually working with changes which risks are worth taking, how much volatility is genuinely acceptable, and what “losing money” means in your specific situation.

I think most investors spend significantly more time researching individual stocks than they spend honestly thinking about their own financial timeline. That imbalance tends to show up eventually – usually at the worst possible time.

The Cash Debate That Nobody Ever Really Finishes

Holding cash has become weirdly controversial.

There’s a version of investing culture that treats uninvested cash like a character flaw. Every dollar sitting in a money market account is a dollar failing to work. Others swing the other way – so scared of missing the next move that they stay almost entirely in equities and then have nothing left to do anything with when prices get genuinely interesting.

I keep coming back to the same simple thing: cash gives you options. And I have never once talked to an investor who regretted having options during a rough market.

If something unexpected happens in your life, you don’t have to sell positions at a bad time to cover it. If the market drops 30%, you can actually put money to work instead of just watching and feeling bad about it. If you want to rebalance, you have room to move.

That’s not a sophisticated thesis. It’s just practical. And practical is underrated.

AI and the Question Investors Keep Avoiding

Almost every portfolio conversation right now ends up at artificial intelligence eventually.

Some of that is deserved. The technology is genuinely changing things and probably will continue to. But investors keep treating two separate questions as if they’re the same question: is the technology real, and are the current prices reasonable?

Those are not the same question.

History has been through this before. The internet was real. It changed everything. It also destroyed a staggering amount of investor wealth because people paid prices during the excitement that couldn’t be justified by anything that happened in the following five years. Being right about the direction and being right about the price are two completely different things – and only one of them actually protects your money.

That distinction is easy to understand in theory. It gets harder to hold onto when everyone around you is making money and you’re the one being cautious.

AI stocks right now are behaving less like investments and more like status symbols – people want exposure regardless of what they’re actually paying for it. The psychology driving that behavior is older than the stock market itself. I wrote about How Luxury Brands Influence Consumer Psychology – and the parallels to how retail investors are currently chasing AI names are uncomfortable to read.

What the Investors Who Actually Last Have in Common

The longer I pay attention to markets, the less convinced I am that investment success comes from having better information than everyone else. News moves in seconds now. Anything that matters gets priced in before most retail investors have finished reading the headline.

What separates people who build real wealth over time from the ones who don’t isn’t the quality of their stock picks. It’s how they behave when things get uncomfortable.

Not panicking when the portfolio looks terrible. Not chasing whatever worked last quarter into an already crowded trade. Not throwing the strategy out after a strong year because suddenly they’re a genius. Not giving up on the whole thing after a bad one.

That sounds simple until real money is actually on the line. Then it becomes surprisingly difficult. Which is exactly why having a real asset allocation strategy for investors – built before the stress arrives, not scrambled together during it – matters more than any individual position ever will.

Eventually the goal stops being about finding the perfect investment.

It becomes about building something solid enough that you’re not checking your phone at 6am with your heart doing something weird, wondering what happened to your retirement account while you were sleeping.

My friend figured that out. Took watching about $8,000 in paper gains evaporate in a single bad week for the message to land.

Most of us need the same lesson. Just hoping you get it a little cheaper than he did.

VeritaLogic publishes independent market and investment analysis for self-directed investors. Nothing here is financial advice – just honest thinking about how markets actually work.