Three years into the AI boom, AI investing stock enthusiasts are facing a question that no amount of research can fully answer: Are we early, or are we late?

Between 2023 and 2025, money poured into anything tagged “AI.” Some investments made substantial returns. Others collapsed. Both happened simultaneously. The winners and losers didn’t always follow predictable logic.

In 2026, the market has matured enough that the answer is no longer “buy anything AI.” The answer is more complicated-which is precisely why it’s more valuable.

Two Different Questions (That Most People Confuse)

When someone asks “should I invest in AI?” they’re typically asking two completely different things without realizing it.

Question 1: Should I own stock in companies built around AI technologies?

Question 2: Should I use AI-powered tools to manage my investments?

These are not the same decision. You can buy AI stocks and manage your portfolio yourself. You can use an AI robo-advisor and own zero AI companies. Understanding which question you’re actually asking determines which strategies make sense.

Most articles blur these questions together. That’s why most investment advice about AI sounds contradictory.

The AI Stock Landscape: Where The Real Money Actually Is

The semiconductor industry remains foundational. Nvidia’s dominance in GPU manufacturing didn’t peak in 2025-it accelerated. According to Nvidia’s Q4 2025 earnings report, the company shipped record data center revenue of $38.1 billion for the fiscal year, with demand continuing to outstrip supply heading into 2026.

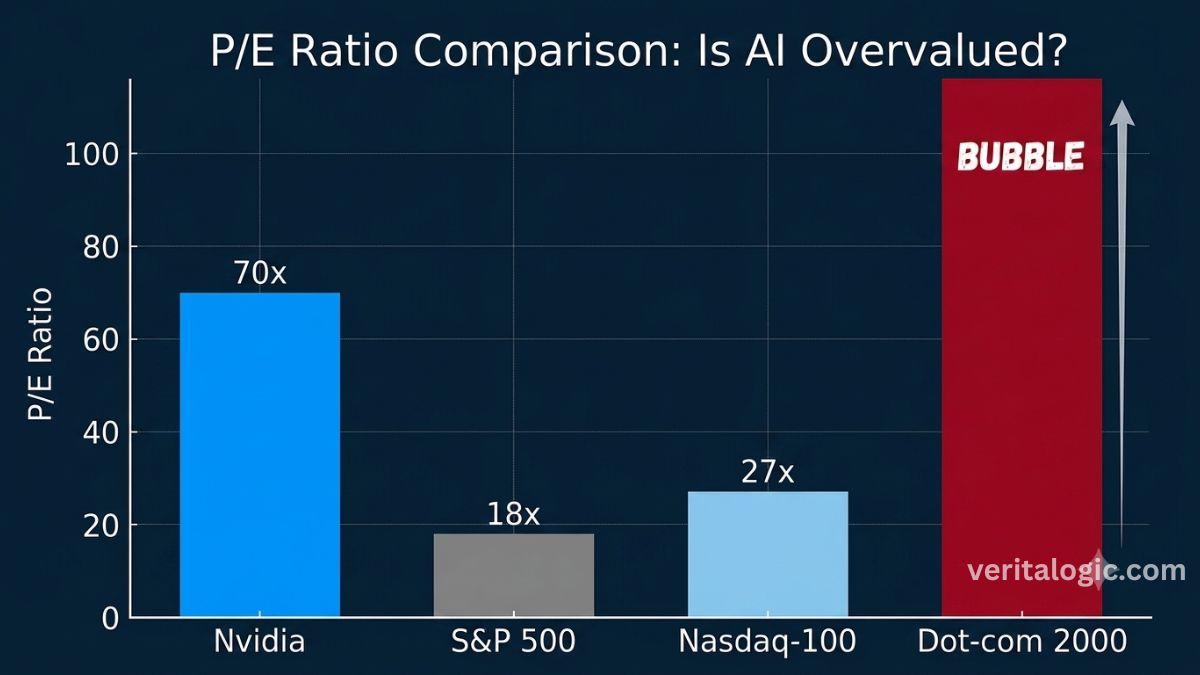

But here’s the uncomfortable reality: Nvidia trades at a forward P/E ratio of approximately 70x. That’s the highest valuation the company has carried since 2021. When an investor buys Nvidia at these multiples, they’re pricing in extraordinary future growth. That growth needs to happen. If it doesn’t, the stock reprices downward sharply.

Cloud infrastructure has become the “picks and shovels” play. Amazon Web Services (AWS) generated $28.2 billion in annual revenue in 2024, with operating margins exceeding 30%. More relevantly for AI: AWS Bedrock (a managed AI service) has become the infrastructure layer that enterprises use to deploy AI models. Microsoft Azure’s AI services, powered by the OpenAI partnership, are following a similar trajectory.

These cloud businesses matter because they get a cut every time someone runs an AI workload. Billions of times per day. That recurring, high-margin revenue is why Microsoft and Amazon stock remain fundamentally more defensible than speculative AI plays.

Enterprise software is where AI actually touches the economy. Palantir, Salesforce, and ServiceNow aren’t building AI from scratch. They’re embedding it into products that hospitals, banks, and logistics companies already use. According to Palantir’s 2025 shareholder letter, the company’s Annual Recurring Revenue (ARR) reached $2.34 billion, with government contracts expanding.

That’s not speculation. That’s revenue.

Alphabet deserves closer scrutiny than most analysts give it. The company has invested in AI infrastructure for over a decade. Its Gemini models now power Google Search, YouTube recommendations, and Workspace products. When OpenAI released ChatGPT, Google’s stock initially sold off on fears that AI would disrupt search revenue. That didn’t happen. Google’s advertising revenue remained resilient through 2025 and into 2026.

Are AI Stocks Already Too Expensive?

This question separates thoughtful investors from speculators.

The AI sector trades at a significant valuation premium to the broader market. Nvidia at 70x P/E. The Nasdaq-100 (heavily weighted toward tech) at 27x P/E. The S&P 500 at 18x P/E.

To contextualize: During the Dot-com bubble (2000), the Nasdaq traded at P/E ratios above 100x. We’re nowhere near that. But we’re also not cheap.

The key metric is PEG ratio (Price-to-Earnings-to-Growth). Nvidia’s 40-50% annual growth rate justifies some valuation premium. But that growth rate is unsustainable indefinitely. At some point, Nvidia matures. When it does, the valuation compresses.

While tech stocks carry their own volatility, precious metals often act as a hedge. For a broader perspective on current market trends, check out our full analysis: Gold vs. Silver: The 2026 Market Story Few Investors Are Watching.

For new money entering AI stocks at current valuations, expect 10-15% annual returns-not the 40-100% gains that early investors captured.

Is that worth it? That depends on your alternatives:

- S&P 500 historical average: 10% annually

- Bonds at 4-5% yield

- Your required rate of return

For conservative investors with shorter time horizons, expensive AI stocks might not make sense. For aggressive, long-term investors, they might.

The mistake is assuming valuation doesn’t matter. It does.

Sources: NVIDIA Investor Relations, Yahoo Finance, Morningstar valuation analysis

What Could Go Wrong? The Risks Nobody Wants To Discuss

The AI investment story has real downside risks that deserve explicit discussion.

Regulatory Risk: The EU’s AI Act is already live. The U.S. is contemplating AI regulation. China restricted AI companies from training on non-approved data. If broad-based regulation tightens access to training data, that breaks the investment thesis for many AI companies. This isn’t coming hypothetically-it’s here and tightening.

Semiconductor Supply: AI infrastructure depends on GPU manufacturing capacity. Nvidia, TSMC, and Samsung are producing record volumes, but capacity remains the constraint. If new competitors suddenly solve this bottleneck, Nvidia’s pricing power disappears. More supply = lower prices = margin pressure.

Development Plateau: What if AI development hits a wall? Current large language models are hitting diminishing returns. Next-generation breakthroughs might require entirely new approaches-or might not come at all. If AI is already “good enough,” the investment case weakens significantly.

Market Correction: The AI sector is crowded. When sentiment shifts from euphoria to skepticism, crowded sectors experience sharp corrections. In 2022, growth stocks fell 40-50%. If AI sentiment reverses, concentrated portfolios could decline similarly.

Bubble Scenario: Low probability, high impact. If AI turns out to be a bubble (like cryptocurrency in 2017), significant capital destruction is possible. The probability is lower than in 2023 because AI actually generates real value. But it’s not zero.

Higher returns come with higher risk. Nvidia offers upside but at valuation risk. AI ETFs provide balanced exposure. Robo-advisors offer stability. The “best” choice depends on your risk tolerance and time horizon.

Understanding these risks doesn’t mean avoiding AI investing. It means sizing your position appropriately and maintaining diversification.

Sources: SEC AI Governance Task Force (August 2025), Bloomberg analysis, regulatory filings

AI ETFs: The Comparison Most Articles Skip

Investing in individual AI stocks requires specific knowledge. ETFs provide diversified exposure through a single trade. But not all AI ETFs are built identically.

Looking for a deeper dive? Danny Sully breaks down the technical nuances of the top AI ETFs for 2026, covering exactly why many investors struggle to pick the right one for their portfolios.

BOTZ (Global X Robotics & AI ETF)

- AUM: $800 million

- Expense Ratio: 0.74%

- Top 5 Holdings: Nvidia (8%), Microsoft (7%), Tesla (6%), Intuitive Surgical (5%), Broadcom (4%)

- 1-Year Return (June 2026): +45%

- 3-Year Return: +18%

- Approach: Broad exposure to robotics, automation, and AI companies

CHAT (Roundhill Generative AI & Technology ETF)

- AUM: $200 million

- Expense Ratio: 0.65%

- Top 5 Holdings: Nvidia (9%), Microsoft (8%), Alphabet (7%), Meta (6%), Broadcom (5%)

- 1-Year Return: +52%

- 3-Year Return: Not available (launched 2023)

- Approach: Companies generating ≥50% of revenue from AI activities

AIQ (iShares Global Tech ETF)

- AUM: $150 million

- Expense Ratio: 0.68%

- Top 5 Holdings: Nvidia (10%), Microsoft (8%), Netflix (5%), Adobe (4%), Broadcom (4%)

- 1-Year Return: +48%

- 3-Year Return: +22%

- Approach: Hybrid tech + AI focus

AI isn’t the only frontier attracting retail capital right now. If you’re interested in other high-growth opportunities, our guide on the space economy is a must-read: SpaceX IPO: A Retail Investor’s Guide.

The Real Comparison:

BOTZ outperformed in 2024-2025 due to broader tech exposure. CHAT has smaller AUM (concentration risk) but lower expense ratio. AIQ offers moderate diversification with reasonable costs.

For most investors, BOTZ or AIQ are better choices than CHAT due to fund stability. Smaller funds (under $100M AUM) carry liquidation risk.

Critical consideration: If you’re a UK or EU investor, check UCITS compliance. Some U.S.-listed funds aren’t eligible for ISAs or SIPPs, creating tax inefficiency.

BOTZ and AIQ offer better fund stability due to larger AUM. CHAT has the lowest expense ratio but smaller asset base. Performance across all three was strong in 2025-2026 due to broad AI sector gains.

Sources: Morningstar (June 2026), fund factsheets, Yahoo Finance

Robo-Advisors: When Automation Makes Sense (And When It Doesn’t)

AI-powered investing platforms-Betterment, Wealthfront, M1 Finance-have genuinely improved at one specific thing: keeping emotional investors out of their own way.

The problem they solve is real. When markets decline 20%, human psychology urges panic selling. Robo-advisors mechanically rebalance, ignore the noise, and maintain allocation targets. Over decades, that discipline compounds into significant outperformance.

According to Morningstar research (2025), investors using robo-advisors had average returns 1.5-2.0% higher annually than self-directed investors, primarily because they didn’t panic sell.

But robo-advisors have genuine limitations:

They don’t handle complexity. If you have equity compensation, business income, real estate holdings, or a nuanced tax situation, a robo-advisor is insufficient. You need human advisory.

They’re backward-looking. They optimize based on historical correlations that can break during market dislocations. During the 2022 rate shock, bonds and stocks fell together-breaking the traditional 60/40 correlation.

They can’t pivot. If life circumstances change-retirement, inheritance, major expense-robo-advisors have limited adaptation ability. A human advisor adjusts. An algorithm follows its programming.

The realistic use case: You’re a disciplined, long-term investor with straightforward financial circumstances. You want automation without weekly thinking. You’re willing to accept adequate returns instead of optimizing for best returns.

For everyone else, robo-advisors solve one problem (emotional discipline) by creating others (reduced flexibility, limited strategy).

Sources: Morningstar research (2025), robo-advisor performance analysis

The Most Expensive Mistakes AI Investors Make

Mistake 1: Chasing the Company Name, Not the Business

In 2023-2024, dozens of small-cap companies added “AI” to press releases and watched stock prices spike. A year later, most had no meaningful AI revenue.

The test: Can the company specifically explain how AI generates revenue today or tomorrow? If the answer is vague (“optimize operations”), it’s marketing. If specific (“AI-powered code generation generates $X revenue”), it’s real.

Example: Palantir’s AI generates revenue through specific government and commercial contracts. A company saying it’s “using AI to improve customer service” is not.

Mistake 2: Trusting AI Trading Signals From Unverified Sources

If you’ve seen accounts promising “AI trading bots with 80% win rates” on social media, they’re scams or vastly misrepresented.

Institutional algorithmic trading systems cost millions and are run by quant funds (Renaissance Technologies, Two Sigma) that have zero incentive to sell them. The fact that something is sold for $49/month tells you everything.

Mistake 3: Concentration Risk Disguised as “AI Focus”

The SEC’s AI Governance Task Force (August 2025) flagged a concerning pattern: AI-generated investment recommendations systematically concentrate in the same five large-cap tech stocks.

When every AI tool recommends the same stocks, those stocks become overpriced. Diversification seems like a cliché until a crowded trade reverses.

Sources: SEC AI Task Force report (2025), market analysis

What Actually Works in AI Investing (Specific Actions)

For Stock Pickers:

- Invest in profitable AI infrastructure (Microsoft, Amazon, Nvidia) rather than speculative plays

- Demand specific revenue metrics (ARR, margins, CAC) before investing

- Diversify across semiconductors, cloud, and enterprise software

- Maintain realistic expectations (10-15% returns at current valuations)

For ETF Investors:

- BOTZ or AIQ for balanced AI exposure

- Avoid funds with <$100M AUM

- Monitor expense ratios (>0.75% is overpriced)

- Rebalance quarterly

For Robo-Advisor Users:

- Set allocation and ignore market noise

- Let the algorithm rebalance without interference

- Check performance annually, not daily

- Accept adequate returns, not optimal ones

Decision tree diagram showing three AI investing approaches: stock picking (invest in Nvidia, Microsoft, Amazon infrastructure), ETF investing (use BOTZ or AIQ with quarterly rebalancing), or robo-advisor automation. Each path includes specific action steps and expected outcomes.

The Bottom Line: Be Skeptical, Stay Disciplined

The AI market is genuinely large and growing. Projections placing the AI market at $2.4 trillion by 2032 (IDC) are plausible. That growth is real.

But “large market” doesn’t mean “all investments in the market succeed.” The Dot-com boom created the internet industry. It also created Pets.com.

The investors who outperformed during the AI boom were those who asked boring questions:

- What does this company actually sell?

- Who pays for it?

- Can I verify the revenue?

- What’s the valuation relative to growth?

- What breaks my thesis?

Those investors maintained discipline, diversified, and sized positions appropriately. In 2026, that same discipline matters more.

The AI opportunity isn’t finding the next 10x stock. It’s avoiding obvious traps while maintaining exposure to real AI infrastructure that generates measurable returns.

That’s not as exciting as finding the next Nvidia at $10 per share. But it’s considerably more likely to work.

Diversification is the key to surviving any market cycle. To explore assets beyond the tech sector, see our latest research here: The Silver Investment Opportunity for 2026.

VeritaLogic publishes independent analysis on investments and personal finance. This article is educational content and should not be considered investment advice. Consult qualified financial advisors before making investment decisions. Data current as of June 2026.

Sources & References:

- NVIDIA Investor Relations (nvidia.com/investor) – Q4 2025 earnings

- Palantir Investor Relations (palantir.com/investor) – 2025 shareholder letter

- Amazon AWS (aws.amazon.com) – 2024 revenue & earnings

- Morningstar (morningstar.com) – ETF research, robo-advisor analysis

- SEC AI Governance Task Force (August 2025 announcement)

- IDC Artificial Intelligence Spending Guide (2025)

- Yahoo Finance – Valuation data, stock performance